blog

blog

For many investors, emerging markets still conjure a reductive caricature: low-income economies, recurring political crises, heavy-handed governments, and returns that haven’t lived up to the hype. While that picture isn’t entirely wrong, it’s materially incomplete. Over the past three decades, the emerging world has shifted from the periphery of the global economy to its fabric: supplying critical components to the AI supply chain, incubating globally competitive consumer platforms, and hosting a growing share of the world’s middle class.

Geopolitical shocks, such as the recent outbreak of large-scale airstrikes in Iran and across the Middle East, illustrate that this progress isn’t linear, and that real risks have the potential to re-price assets quickly. However, from a long-term structural perspective, this evolution remains directionally intact and its ramifications for the role that emerging markets equities plays in a diversified portfolio along with its implementation should be revisited.

In this paper, we look back over several decades to show how the composition and character of emerging markets have changed. We then highlight three themes that matter today: the role of companies like TSMC and its ecosystem at the heart of the AI supply chain; the rise of wealth and domestic demand; and the question of whether typical EM exposures are delivering the diversification benefits North American investors expect.

Ultimately, we argue that this is a sensible moment to re-examine emerging markets, emphasizing quality businesses over benchmarks, innovators with local roots, diversification beyond China and India, and a genuinely all‑cap approach that reflects the true breadth of the opportunity set.

From frontier to fabric: A brief modern summary of emerging markets

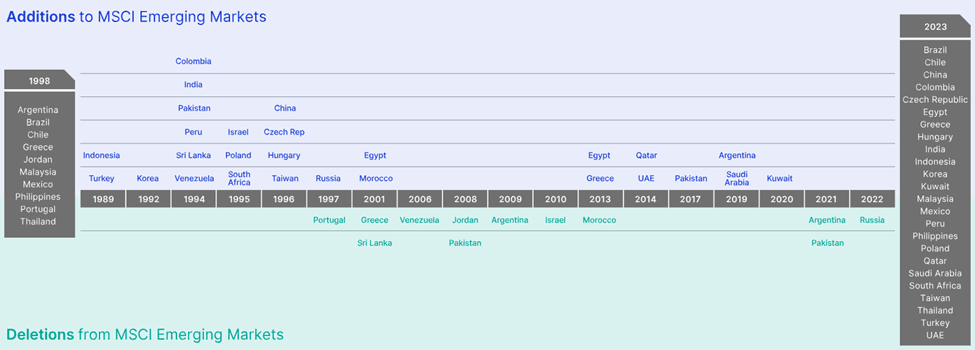

Emerging markets of the 1990s were largely defined by crises: volatile capital flows, fragile banking systems, sharp currency devaluations, and contagion are all associated with the Mexican peso crisis of 1994, the Asian Financial Crisis of 1997, and the Russian default crisis of 1998. Bill Browder’s Red Notice provides one of the more colourful accounts of the dangers and swings an emerging market investor had to endure in that era. But it was also a period in which many of today’s EM heavyweights began their ascensions, transforming what had been a predominantly Latin American universe heavy on commodities, with Asia largely at the periphery.

Figure 1: A dynamic geographic landscape

Source: MSCI

China’s entry into the World Trade Organization in 2001 was transformative, accelerating its integration into global trade and supply chains. The rise of the BRICs (Brazil, Russia, India, and China), supported by a powerful commodity supercycle, reinforced the notion that emerging markets were primarily about resource exports and investment-heavy growth models.

Since the global financial crisis, however, the EM opportunity set has steadily diversified. Asian markets such as Taiwan, South Korea, and India have gained prominence, driven by technology, electronics, and services rather than commodities. Many emerging economies have strengthened monetary policy frameworks, moved toward more flexible exchange rates, and developed local currency bond markets that reduce their dependence on foreign currency borrowing.

More recently, China’s growth slowdown, the explosion in AI-related investment, and a reshaping of the geopolitical map including the most recent airstrikes in the Middle East have presented new risks and opportunities for investors to consider.

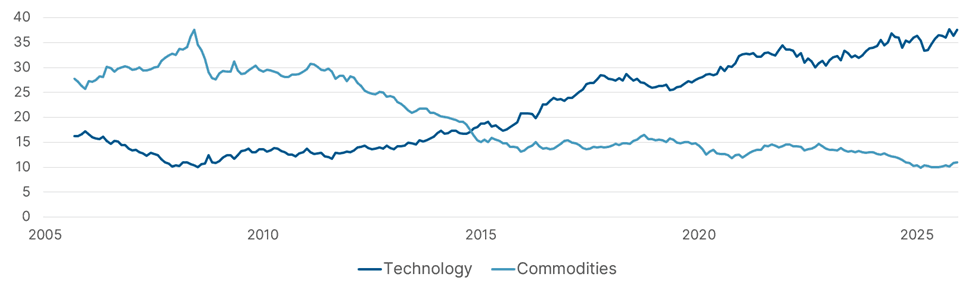

Figure 2: Shovels out, servers in

MSCI EM Index segment composition over time (%)

As of December 31, 2025

Source: MSCI, Mawer

Country evolution has gone hand in hand with changes in sector composition. The EM indices of the late 1990s and 2000s were dominated by energy, materials, and state-owned banks. While those sectors remain important, technology and consumer sectors account for a much larger share of the universe today. Economies that were once mainly cyclical exporters now host critical nodes in global value chains—notably in semiconductors, electronics, and manufacturing. Domestic markets have deepened through rising urbanization and digital adoption.

The substitution of lower-cost, capital intensive, often state-owned or heavily state-influenced companies exhibiting generally lower returns on capital (think: Vale, Gazprom, and Petrobras) for more shareholder-aligned, scalable, differentiated, and higher-return businesses (think: Tencent, TSMC, HDFC) means that the character of the emerging markets universe—while still incredibly varied and without downplaying important risks—has dramatically improved in terms of quality over the years.

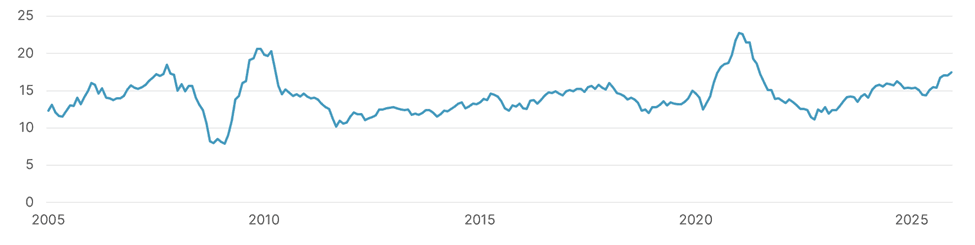

This begs two questions: why haven’t valuations in emerging markets reflected the shift toward a higher-quality universe? And for Canadian investors specifically, does a shift from what once may have been characterized as a homogenous, commodity-driven universe highly correlated with our own domestic stock market mean that emerging markets now provide a much better value proposition in terms of diversification benefits?

Figure 3: Apples to apples?

MSCI EM Index – Trailing P/E

As of December 31, 2025

Source: MSCI , Mawer

All roads lead to TSMC

Jack Nicholson as Irish mob boss Frank Costello has a great line to open Martin Scorsese’s The Departed: “I don’t want to be a product of my environment. I want my environment to be a product of me.”

Fifty years ago, authorities in Taiwan adopted a similar mindset. Taiwan’s economy in the 1970s was largely based on agriculture and low-end, thin-margin manufacturing. In a stroke of masterful foresight, the government made strategic investments in developing technological capabilities—specifically semiconductors—as a pathway to a more secure and wealth-creating economy. With a lack of intellectual property in integrated circuit design, the emphasis was on manufacturing. This ultimately resulted in the formation of a pure-play foundry under Morris Chang’s leadership: TSMC.

An unusual model at the time, TSMC allowed chip designers to outsource production and focus on architecture rather than fabrication. That division of labour, supported by consistent re-investment and an engineering‑driven culture, helped turn a small island economy into the indispensable hub of the global semiconductor industry.

But beyond TSMC, an entire ecosystem of specialist suppliers and service providers has grown up in Taiwan and across the broader region. Companies that design and install clean‑room environments, supply niche equipment, manage critical utilities, or provide maintenance and engineering services have effectively become extensions of TSMC’s own capabilities. Acter Group, for example, focuses on high‑specification mechanical and electrical engineering for fabs and other advanced facilities. Numerous smaller companies provide materials, consumables, and on‑site technical support highly tailored to TSMC’s processes. Individually, these businesses may be small or mid‑cap in size. But collectively, they form an industrial cluster that is nearly impossible to replicate or displace. And while they operate in hyper-specialized niches, many of them command the same types of dominant market shares and competitive advantages as TSMC, thereby providing attractive investment opportunities.

The most recent phase of AI adoption has highlighted another pressure point in the chain: memory. Training and running large models is extraordinarily memory‑intensive. Over the last several months, memory has become a critical bottleneck, with supply struggling to keep up with demand for AI‑specific configurations. This has elevated the strategic importance of memory manufacturers and packaging specialists, many of which are based in emerging Asia, and has reinforced how tightly coupled the various parts of the semiconductor stack have become.

Trust is a critical, if less visible, asset in this ecosystem. When a company like Nvidia designs a new GPU, it is not simply buying anonymous capacity; it is entrusting partners with intellectual property, product timelines, and reputational risk. Specialist testing and packaging firms such as King Yuan Electronics play a central role here, probing and validating chips before they‘re shipped onward and ensuring that devices perform to specification under demanding conditions. Any systematic failure at this stage can cascade through the value chain, from data‑centre operators down to end users. As AI workloads become more complex and the cost of downtime rises, the value of reliable, deeply embedded partners only increases.

For investors in emerging markets, the question is not simply whether AI investment will hit a speedbump in demand, but where it is genuinely improving business quality by reinforcing moats. In many parts of the semiconductor value chain, the stakes are high and rising. When that happens, accumulated process knowledge, long‑dated customer relationships, and a culture of operational excellence are hard to clone.

Wealth effects in EMEA

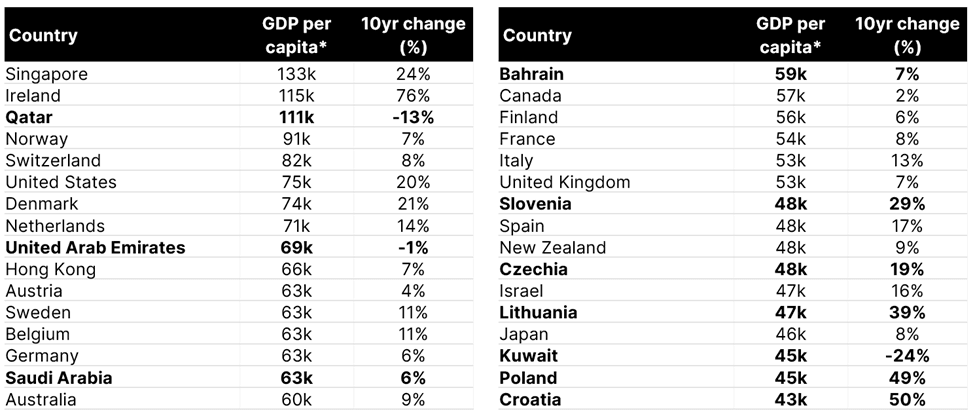

Though MSCI controls the classification of what constitutes an emerging market country, the picture of low-income economies climbing the development ladder is hardly representative of the whole universe. Some of the most interesting changes in recent years have occurred at the upper end of the spectrum: countries that are wealthy on a GDP per capita basis but still evolving rapidly in terms of institutions, capital markets, and consumption patterns. Many of these sit in the geographic “region” of EMEA: Europe, the Middle East, and Africa—hardly a homogeneous area!

The table below lists countries in descending order of GDP per capita, with emerging markets countries in bold. While the presence of many of the Gulf states may be expected given their hydrocarbon wealth, the remarkable rise in incomes in Eastern Europe from the likes of Slovenia, Lithuania, and Poland means that incomes in those countries now rival those of developed markets such as Japan, New Zealand, and the UK.

Figure 4: Rising fortunes, emerging wealth

GDP per capita

As of 2024

*PPP (constant 2021 international $); excludes countries with populations below 2 million

Source: World Bank, Mawer

In the Gulf, what’s changing is not income levels so much as the orientation of policy and capital. Governments have become increasingly capital‑market friendly, using public listings and stake sales not to plug fiscal holes, but to deepen local markets, improve governance, and broaden ownership. IPOs of government‑linked assets, such as toll‑road operator Salik in Dubai, reflect this shift. In effect, parts of the Gulf are moving from resource‑rich states with thin markets toward more balanced economies with a growing base of local and international investors. An extended period of conflict and significant geopolitical uncertainty could reshape long-term risk premia and discount rates; tail risks have indeed increased over the past weeks. But we continue to believe that positive developments in Gulf states remain a theme worth following.

In Eastern Europe, as households move increasingly to middle-income levels, spending and consumption patterns tend to shift from basic necessities to more discretionary categories: better food, modern retail formats, health and wellness, education, leisure, and digital services. Over time, some of these discretionary items become de facto staples: gym memberships, private healthcare plans, or e‑commerce platforms that households come to rely on. Companies in Poland such as Dino Polska, which has built a modern proximity grocery network serving smaller towns, or Benefits Systems, which aggregates employee benefits and fitness packages, are examples of businesses that ride this transition from basic to aspirational to everyday. Baltic Classifieds, which operates leading online marketplaces in Lithuania and Estonia, is a great example of how even relatively small economies can support dominant digital platforms once incomes and internet penetration reach a certain threshold, with room to increase monetization given take-rates far below those of their developed market peers.

For investors, these developments broaden the definition of what “emerging” means. It’s no longer only about low‑income countries racing to catch up. Solid starting income levels, improving policy environments, and evolving consumption patterns can be fertile ground for quality companies with durable, locally rooted franchises—especially so when AI and other geographies (e.g. China and India) swallow so much of emerging markets investors’ attention.

Think wider

One of the main reasons investors allocate to emerging markets is diversification. On paper, EM allocations should offer exposure to growth drivers, policy regimes, and currencies that are different than a US or developed market-centric portfolio. In practice, however, large swaths of the emerging markets universe (by market cap) underdeliver in this regard.

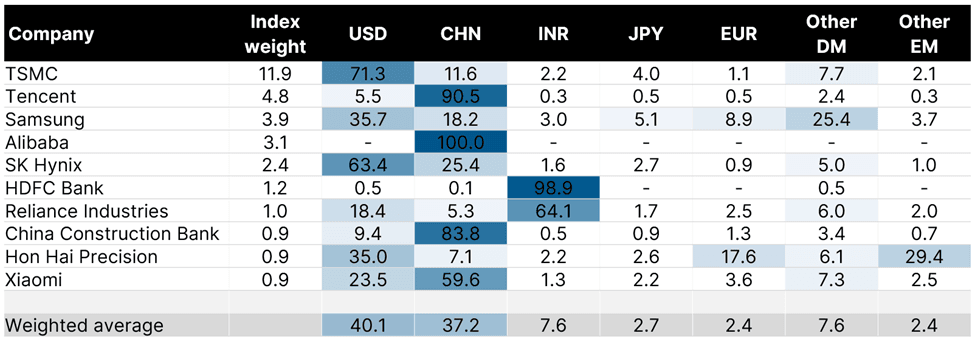

Figure 5: Intended diversification?

Revenue exposure by currency

As of December 31, 2025. Top 10 constituents of the MSCI Emerging Markets Index

Source: Mawer, MSCI, Xpressfeed

Consider the top constituents of the MSCI Emerging Markets Index. In breaking down their revenues by currency, the exposure is heavy to the US dollar and to two admittedly key markets: China and India. But the economic exposure to other emerging markets countries is extremely sparse. And given some of the aforementioned EM landscape shifts over the past few decades, with a greater preponderance of technology-linked companies, these revenues may behave more similarly to those from an already tech-heavy S&P 500 portfolio allocation. Correlation statistics can obscure this nuance because they summarise the behaviour of entire indices over long periods. The underlying economic exposures are just as important: where companies earn their revenues and how dependent they are on the same global demand drivers that move US markets.

For investors seeking genuine diversification, the question is therefore not only “How much EM should we own?” but additionally a much more nuanced “What kind of EM should we own?” To get the biggest bang for your buck from an EM allocation, investors should seek a broad canvas of genuine emerging markets exposure.

How to invest in EM today: Principles, not predictions

The case for emerging markets today is less a call on a particular macro outcome (e.g., faster growth, a weaker US dollar, or a specific policy shift in one country), and more a case for how to participate in a more diverse, more systemically important set of companies. And this starts with an emphasis on businesses rather than betas.

First, prioritise quality over broad index beta. Dispersion between good and bad businesses in EM remains wide. Companies with durable competitive advantages, sensible balance sheets, and disciplined capital allocation are better placed to turn uneven growth into shareholder returns. Portfolios built around these firms will usually look very different than the benchmark: less tilted to state‑influenced incumbents, more skewed to enterprises that can reinvest at high incremental returns.

Second, diversify beyond AI, China, and India. All three are central to any EM portfolio, will remain important drivers of returns and risk, and offer lots of attractive investment opportunities. But a portfolio that equates EM with those two countries misses a growing set of opportunities in the Gulf, Eastern Europe, Southeast Asia, Latin America and frontier‑to‑EM markets. These regions offer different policy cycles, different sector mixes, and different relationships to global trade. Spreading exposure across them can improve resilience to country‑specific shocks and reduce the risk that a single regulatory or macro event dominates EM performance.

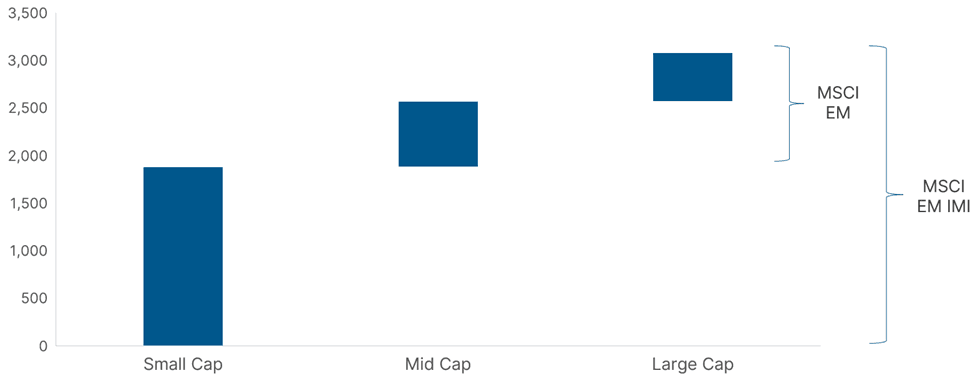

Figure 6: Think wider: An all-cap approach

Number of index constituents

As of December 31, 2025

Source: MSCI

Third, adopt a genuinely all-cap approach. Many of the businesses that best reflect EM’s evolving opportunity set—niche suppliers in the semiconductor ecosystem, dominant regional platforms, or local champions in rising‑income economies—sit outside the large‑cap core of standard indices. Smaller and mid‑sized companies can offer more direct exposure to domestic themes and earlier‑stage innovation, albeit with higher idiosyncratic risk. [Not to mention for bottom-up investors, the delicious prospect of uncovering hidden gems!]

The table below provides a further illustration of how the smaller end of the capitalization spectrum provides a very different opportunity set. A thoughtfully constructed all‑cap portfolio that’s grounded in quality and valuation discipline can capture this breadth while still managing liquidity and governance considerations.

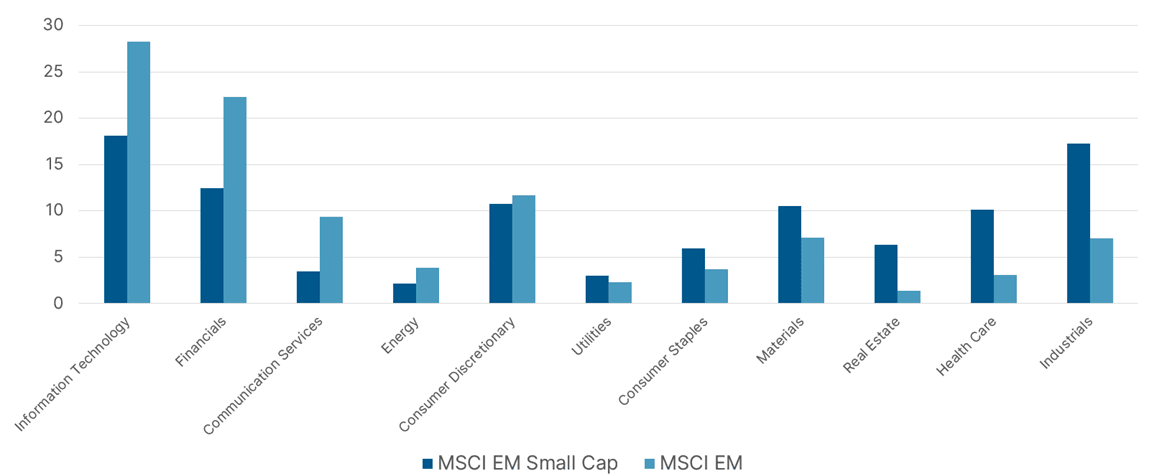

Figure 7: Smaller caps, local focus

Distribution of sector weights (%)

As of December 31, 2025

Source: MSCI

Finally, seek out domestic champions whose economics are less directly hostage to tariffs and cross‑border frictions. Companies whose revenues are primarily local are not immune from global shocks, but they are often one step removed. Tencent Music, for instance, operates in a challenging Chinese macro and regulatory environment, yet its core business of music streaming still has room for increased penetration, improved monetisation, and is likely viewed by its customers as a staple. The value of its platform, catalogue, and user relationships depends less on a booming Chinese economy and more on steady progress in converting a large base of listeners into paying customers. Done sensibly, that kind of operational improvement can create shareholder wealth even against a muted domestic backdrop.

Similarly, FPT Digital Retail in Vietnam illustrates how EM companies can take advantage of weaker competition and fragmented markets. As modern drug store and retail chains expand, they displace informal channels, improve availability and quality, and benefit from scale in procurement and logistics. In this type of environment, a capable operator can compound earnings by opening new stores, deepening customer relationships, and gradually formalising everyday spending, without relying on heroic assumptions about macro conditions.

Taken together, these principles point toward a way of investing in EM that’s less about making a single call on the asset class and more about assembling a collection of resilient, cash‑generative businesses across a changing map.

In a world where emerging markets are increasingly integral to the global economy and the cost of operational missteps is rising, opportunity lies not in owning emerging markets, but in owning the right mix of businesses within them.

Disclaimers

This publication is solely intended for informational purposes and should not be construed as individualized investment advice, research, or a recommendation to buy, sell or hold specific securities. Information provided reflects current views based on data available at the time or writing and may change without notice. Mawer Investment Management Ltd. and/or its clients may hold positions in the securities mentioned, which may create a potential conflict of interest. While efforts are made to ensure accuracy, Mawer Investment Management Ltd. does not guarantee the completeness or accuracy of this information and disclaims liability for any reliance placed on the publication. Mawer Investment Management Ltd. is not liable for any damages arising out of, or in any way connected with, its use or misuse.

The MSCI information may only be used for your internal use, may not be reproduced or disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)